Technology

Asia Pacific Gaming Peripherals Market Share & Growth, 2033

Asia Pacific Gaming Peripherals Market Size

The Asia Pacific gaming peripherals market size was valued at USD 1493.12 million in 2024 and is anticipated to reach USD 1610.48 million in 2025 from USD 2950.11 million by 2033, growing at a CAGR of 7.86% during the forecast period from 2025 to 2033.

The Asia Pacific gaming peripherals market encompasses a wide range of hardware devices including gaming keyboards, mice, headsets, controllers, and VR accessories designed specifically for enhanced gaming experiences. Countries such as China, Japan, South Korea, India, and Australia are witnessing rapid expansion in both casual and professional gaming sectors, which is fueling product innovation and brand competition. A significant catalyst behind this growth is the increasing penetration of online and mobile gaming platforms, which have created new avenues for peripheral integration beyond traditional PC setups. According to Newzoo, the Asia Pacific region accounted for more than 45% of the global games market revenue in 2023, with China alone contributing over USD 40 billion in game-related spending. The rise in esports events and streaming content across platforms like Twitch and Douyu has further intensified consumer demand for premium-grade gaming gear that enhances performance and immersion.

MARKET DRIVERS

Surge in Competitive and Esports Gaming Activities

One of the primary drivers influencing the Asia Pacific gaming peripherals market is the exponential growth of competitive and esports gaming activities. The region has become a global epicenter for organized gaming tournaments, live-streamed competitions, and professional gamer sponsorships, all of which necessitate high-precision input devices and immersive audio equipment. China, in particular, remains home to some of the largest esports leagues globally, including the League of Legends Pro League and the King Pro League. These events attract millions of spectators and require players to utilize top-tier peripherals optimized for latency reduction, durability, and responsiveness. Similarly, South Korea’s well-established esports infrastructure fosters a continuous demand for high-end mechanical keyboards, ultra-fast mice, and noise-canceling headsets. In Japan, the government-backed Japan eSports Union has been actively promoting regulatory frameworks to legitimize professional gaming, encouraging brands to develop specialized product lines catering to this rising demographic. Additionally, universities and gaming academies across the Philippines, Malaysia, and Thailand are now offering formal esports training programs, further embedding gaming peripherals into mainstream education and youth culture.

Rising Popularity of Streaming and Content Creation Platforms

The second major driver propelling the Asia Pacific gaming peripherals market is the growing influence of livestreaming and digital content creation platforms. Platforms such as Twitch, YouTube Gaming, Douyu, and Kuaishou have transformed how individuals engage with video games, turning millions into creators who rely on high-fidelity microphones, webcams, RGB lighting systems, and programmable macro keys to enhance their production quality. According to StreamElements, in 2023, Asian broadcasters collectively logged over 700 million hours of streamed content, indicating a dramatic shift in media consumption and creator economies. Many of these creators invest heavily in premium peripherals such as studio-grade headsets, customizable mechanical keyboards, and multi-button gaming mice to improve interactivity and viewer engagement. Meanwhile, in South Korea, where streaming is deeply integrated into pop culture, influencers often collaborate with peripheral brands to launch signature editions, driving both visibility and sales.

MARKET RESTRAINTS

High Cost of Premium Gaming Peripherals

A significant restraint affecting the Asia Pacific gaming peripherals market is the relatively high cost of premium-grade accessories, which limits accessibility for budget-conscious consumers. Unlike standard computer peripherals, gaming-focused products often feature advanced components such as optical switches, high-polling rate sensors, and proprietary software ecosystems—all of which contribute to elevated price points. In countries like Indonesia, Vietnam, and the Philippines, where average per capita income remains lower compared to developed markets, affordability becomes a key barrier to adoption. While mid-range and entry-level alternatives exist, they often compromise on build quality, customization features, and long-term durability factors that are highly valued by serious gamers. Local retailers report that despite strong interest in high-performance gear, only a fraction of consumers can justify the cost given other financial priorities.

This pricing disparity restricts market penetration among younger demographics and casual gamers, who form a substantial portion of the regional player base. Additionally, counterfeit or grey-market products have gained popularity due to their lower costs, posing a challenge to legitimate brands trying to establish a foothold in certain parts of the region. Until pricing strategies evolve to better align with regional purchasing power, high-cost barriers will remain a persistent challenge for the widespread adoption of premium gaming peripherals in the Asia Pacific market.

Short Product Lifecycles and Rapid Technological Obsolescence

Another critical constraint hindering the growth of the Asia Pacific gaming peripherals market is the rapid pace of technological innovation, which leads to short product lifecycles and frequent obsolescence. Unlike traditional consumer electronics such as smartphones or televisions, gaming peripherals face constant pressure to integrate new features such as adaptive haptics, AI-driven macros, and wireless latency reduction. According to ABI Research, the average lifecycle of a high-end gaming mouse or keyboard is less than two years, forcing consumers to upgrade frequently to keep up with market trends.

This accelerated innovation cycle disproportionately affects price-sensitive markets in the Asia Pacific region, where users may not afford to replace gear at such intervals. For instance, in India and Thailand, many gamers still rely on older-generation peripherals due to limited disposable income and slower replacement cycles. OEMs and retailers note that while there is high awareness of cutting-edge models, actual purchase conversion remains low unless bundled with promotions or discounts.

MARKET OPPORTUNITIES

Expansion of Cloud Gaming and Cross-Platform Compatibility

An emerging opportunity shaping the Asia Pacific gaming peripherals market is the rapid rise of cloud gaming services and the push toward cross-platform compatibility. Companies like NVIDIA GeForce Now, Xbox Cloud Gaming, and Sony’s PS Plus Premium are expanding their presence in the region, enabling users to access high-end games without requiring expensive PCs or consoles. This transition has created a demand for peripherals that can seamlessly function across multiple platforms, including smartphones, tablets, laptops, and hybrid gaming devices. Manufacturers are responding by developing versatile input devices such as Bluetooth-enabled controllers, modular keyboards, and universal dongles that support Windows, Android, and iOS simultaneously. Brands like Razer and HyperX have already introduced peripherals tailored for cross-platform use, enhancing user flexibility and engagement.

Additionally, the proliferation of hybrid gaming devices such as the Steam Deck and Nintendo Switch OLED has spurred demand for compatible accessories that complement portable gameplay. Gamers in urban centers like Singapore, Tokyo, and Seoul are increasingly adopting lightweight, portable peripherals that sync effortlessly with their mobile and console environments.

Growth of Niche and Customizable Gaming Gear Markets

Another promising avenue for the Asia Pacific gaming peripherals market lies in the rising demand for niche and highly customizable gaming gear. Gamers today seek products that reflect personal style, ergonomic preferences, and performance-specific enhancements, creating opportunities for brands to differentiate through aesthetic design, modularity, and user-defined configurations. According to Grand View Research, the global customizable gaming peripherals segment is expected to grow at a CAGR of over 12% between 2023 and 2030, with Asia Pacific being a major contributor to this trend.

Japan stands at the forefront of this movement, with brands like Keychron and Drop collaborating with local designers to offer limited-edition mechanical keyboards inspired by anime, streetwear, and retro computing aesthetics. Similarly, in South Korea, custom-built PC gaming shops in cities like Seoul allow users to personalize every component—including keyboards and mice—based on color schemes, switch types, and even engraved details.

MARKET CHALLENGES

Intense Market Saturation and Brand Proliferation

A pressing challenge facing the Asia Pacific gaming peripherals market is the intense saturation caused by an influx of both international and local brands vying for consumer attention. The market has become highly fragmented, with numerous players offering similar product categories at varying price points, making differentiation difficult. According to Gartner, over 200 distinct gaming peripheral brands were active in the Asia Pacific region in 2023, ranging from established global names to emerging domestic startups.

This crowded landscape places immense pressure on marketing budgets and product innovation cycles. Global leaders like Logitech, Corsair, and Razer must compete against agile, cost-effective local brands such as Redragon (Australia), Qck (India), and Vortexgear (Philippines), which leverage regional manufacturing capabilities and localized branding to capture market share. Additionally, white-label manufacturers on e-commerce platforms are flooding the market with budget-friendly options, further complicating consumer decision-making processes and diluting brand loyalty.

Regulatory and Trade Barriers Affecting Supply Chains

Another critical challenge impacting the Asia Pacific gaming peripherals market is the evolving landscape of trade regulations, tariffs, and import restrictions that affect supply chain efficiency and product availability. The region’s geopolitical volatility, particularly between China, the United States, and neighboring ASEAN countries, has led to unpredictable trade policies that disrupt logistics networks and increase operational costs for manufacturers and distributors alike. For instance, India’s customs authorities imposed stricter import duties on electronic goods in 2023, including gaming peripherals, aiming to promote domestic manufacturing under its Make in India initiative. According to the Indian Ministry of Electronics and Information Technology, these measures led to a 25% increase in the landed cost of imported peripherals, directly affecting consumer access and brand profitability. Similarly, in Indonesia, regulatory mandates requiring localization certifications for imported electronics have delayed product launches and inflated compliance expenses for foreign vendors.

These trade complexities are compounded by logistical bottlenecks, especially in island nations like the Philippines and Malaysia, where last-mile delivery infrastructure struggles to meet e-commerce demands. Distributors report higher lead times and inconsistent inventory availability, affecting customer satisfaction and market expansion plans. Additionally, shifting data privacy laws in countries such as Australia and Japan impose additional compliance burdens on smart-enabled peripherals that collect user data, further complicating product development and distribution strategies.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

7.86% |

|

Segments Covered |

By Product Type, Gaming Device, Technology, Distribution Channel and Region. |

|

Various Analyses Covered |

Global, Regional and country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

Logitech International S.A., Razer, Inc., Cooler Master Technology, Inc., Eastern Times Technology Co., Ltd. (Redragon), Thermaltake Technology Co., Ltd., Guillemot Corporation S.A., Shenzhen Rapoo Technology Co., Ltd., Sennheiser Electronic GmbH & Co. KG, Anker Innovations Limited, Kingston Technology Company, Inc., |

SEGMENTAL ANALYSIS

By Product Type Insights

The gaming headsets segment dominated the Asia Pacific gaming peripherals market with 28.4% of share in 2024 due to the growing emphasis on immersive audio experiences across both casual and competitive gaming environments. Gamers increasingly rely on high-fidelity sound for positional awareness, voice communication, and content consumption in multiplayer and esports scenarios.

According to Futuresource Consulting, over 65% of PC and console gamers in South Korea and Japan use dedicated gaming headsets regularly, driven by the region’s strong esports culture and streaming habits. In China, where online multiplayer games such as Honor of Kings and PUBG Mobile are immensely popular, headset adoption has surged due to increased in-game voice chat requirements and social connectivity features. Additionally, brands like HyperX, Razer, and SteelSeries have expanded their product portfolios to include budget-friendly yet feature-rich headsets tailored for emerging markets like India and Southeast Asia. As per IDC, in 2023, gaming headset sales in India grew by 35% year-on-year, largely influenced by the rise in live-streaming platforms such as Twitch and YouTube Gaming. The increasing integration of noise cancellation, surround sound simulation, and RGB lighting further enhances consumer appeal, reinforcing the headsets category as the largest contributor to the regional market.

The gaming mice segment is projected to grow with a CAGR of around 11.4% in the next coming years. This rapid expansion is fueled by the increasing demand for precision control in PC gaming among players engaging in first-person shooters, real-time strategy games, and simulation-based titles.

China leads this growth trajectory, where a significant portion of the estimated 700 million gamers prefer mechanical keyboards and high-performance mice tailored for responsiveness and durability. According to Niko Partners, nearly 40% of Chinese PC gamers upgraded their input devices in 2023, with many opting for ultra-lightweight mice featuring adjustable DPI, programmable side buttons, and advanced sensor technologies.

In India, the shift toward professional esports training centers and home-based gaming setups has also contributed to rising mouse demand. The Esports Federation of India reported that organized PC gaming events grew by 50% in 2023, prompting enhanced peripheral investments from competitive players. Furthermore, e-commerce platforms such as Flipkart and Amazon.in witnessed a surge in cross-border listings for branded gaming mice, indicating strong consumer interest despite price sensitivity.

Japanese and Korean manufacturers are responding with innovations in optical tracking, weight customization, and wireless capabilities, ensuring compatibility with evolving desktop and laptop configurations. With continued advancements in ergonomics and performance optimization, the gaming mice segment remains one of the most dynamic areas within the Asia Pacific gaming peripherals landscape.

By Gaming Device Type Insights

The PC (desktop/laptop) segment led the Asia Pacific gaming peripherals market with dominant share in 2024. In China, the Ministry of Culture and Tourism recorded over 650 million PC gamers in 2023, contributing significantly to the demand for premium gaming gear. Tencent and NetEase, two major domestic game developers, continue to release new titles exclusively for PC, reinforcing the platform’s relevance in the ecosystem. Moreover, universities and corporate offices are integrating gaming laptops into digital media curricula and entertainment lounges, further expanding peripheral demand.

The gaming consoles segment is likely to grow with a CAGR of 9.7% from 2025 to 2033 owing to the proliferation of next-generation consoles such as PlayStation 5, Xbox Series X/S, and Nintendo Switch OLED, which have gained traction in both mature and developing markets. Japan remains a core hub for console gaming, with Sony and Nintendo actively releasing exclusive titles and enhancing cloud streaming capabilities to attract new audiences. Meanwhile, in South Korea, Microsoft’s introduction of Xbox Cloud Gaming has enabled users to stream console-quality games on mobile and tablet devices, increasing reliance on compact and adaptive controllers. Additionally, companies like Scuf Gaming and PowerA are launching localized controller variants with ergonomic improvements and customization options tailored for Asian consumers.

By Technology Insights

The wired technology segment was accounted in holding 56.4% of the Asia Pacific gaming peripherals market in 2024. Despite the rising popularity of wireless alternatives, a large portion of the gaming community still prefers wired peripherals for their perceived reliability, lower latency, and consistent power supply where factors deemed crucial in competitive and high-intensity gaming environments. South Korea exemplifies this trend, where professional esports teams and tournament organizers predominantly use wired mice and keyboards to ensure minimal input lag and maximum responsiveness. In China, the National Electronic Sports Association mandates strict hardware guidelines for sanctioned events, favoring wired connections due to concerns about signal interference and battery life reliability in wireless models. Moreover, in cost-sensitive markets like India and Indonesia, wired peripherals remain the preferred choice among budget-conscious gamers who prioritize affordability over mobility. Furthermore, many educational institutions and public gaming centers opt for durable, plug-and-play wired solutions to minimize maintenance costs and technical complications.

The wireless technology segment is expected to grow at the fastest CAGR of 13.2% from 2025 to 2033. This rapid expansion is being propelled by continuous advancements in wireless connectivity, including low-latency Bluetooth protocols, proprietary RF solutions, and improved battery life, all of which have addressed previous concerns regarding performance and reliability.

China is leading the charge, with a surge in demand for wireless gaming headsets, mice, and controllers that support the country’s growing mobile and hybrid gaming ecosystem. According to IDC, in 2023, over 45% of newly purchased gaming mice in China featured dual-mode wireless connectivity (Bluetooth + dongle), up from just 15% in 2020. Similarly, Japanese tech firms like Astro Gaming and Elecom are introducing lightweight, noise-canceling wireless headsets designed specifically for remote work and gaming convergence.

India is also experiencing a boom in wireless adoption, particularly among students and young professionals who value portability and aesthetics. Amazon India reported a 60% year-over-year increase in wireless keyboard and mouse combo sales in 2023, with influencer reviews and bundled promotions driving impulse purchases. Additionally, in Singapore and Australia, the rise of BYOD (bring your own device) policies in gaming lounges and co-working spaces has led to greater demand for peripherals that seamlessly switch between multiple devices.

By Distribution Channel

The online distribution channel dominated the Asia Pacific gaming peripherals market with prominent share in 2024. In China, Tmall and JD.com accounted for over 75% of all gaming peripheral sales in 2023, according to iResearch, thanks to aggressive marketing campaigns, fast delivery networks, and integrated payment gateways that facilitate seamless transactions. Similarly, in India, Amazon.in and Flipkart reported a 50% year-on-year increase in gaming accessory sales, driven by festive season discounts and easy EMI financing options targeted at youth consumers.

Southeast Asian countries like Vietnam and Thailand have also seen a surge in online shopping, with local platforms such as Shopee and Tokopedia offering localized payment methods and attractive bundling deals. The Esports Federation of the Philippines noted a 40% increase in online purchases of branded gaming mice and headsets among amateur players preparing for online tournaments hosted via Discord and Zoom. Moreover, direct-to-consumer brand stores operated by companies like Razer, Corsair, and Logitech have gained traction in the region, allowing customers to access limited-edition products and personalized configurations without intermediaries.

The offline distribution channel is projected to grow at a steady CAGR of 7.8% from 2025 to 2033. This growth is being driven by experiential retail, product demonstrations, and the strategic expansion of specialty electronics and gaming stores that cater to hands-on consumers seeking tactile engagement before purchase.

In Japan, electronics retailers such as Bic Camera and Sofmap have dedicated sections for high-end gaming peripherals, allowing shoppers to test ergonomics, button layouts, and actuation forces before committing to a purchase. Similarly, in South Korea, the resurgence of PC café chains like GotoPC and SpeedMate has revitalized interest in physical retail touchpoints, where users can trial peripherals before buying personal units. Some cafes even offer in-house branding partnerships with manufacturers like Razer and ASUS, creating localized product lines that resonate with regional preferences. In emerging markets like Indonesia and India, tier-2 and tier-3 cities are witnessing a rise in small-scale electronics retailers stocking branded and generic gaming accessories to meet grassroots demand. These shops provide after-sales support, warranty processing, and product swaps, which are often lacking in online-only setups.

COUNTRY-LEVEL ANALYSIS

China was the top performer in the Asia Pacific gaming peripherals market by capturing 34.4% of share in 2024. As the world’s most populous nation with one of the highest numbers of digital gamers globally, China’s influence on the peripheral ecosystem is substantial and multifaceted.

According to the China Internet Network Information Center (CNNIC), the country had over 650 million online gamers in 2023, with a significant portion engaged in PC and mobile-based gaming. This vast player base drives consistent demand for high-performance keyboards, mice, headsets, and controllers. Moreover, the government-backed esports initiatives, including the establishment of specialized training academies and national leagues, have reinforced the need for premium-grade peripherals among aspiring professionals. Companies like Tencent, NetEase, and Xiaomi have launched localized gaming hardware lines tailored to domestic preferences, while global brands such as Razer and Logitech have expanded their retail presence through partnerships with major e-commerce platforms like Tmall and JD.com. The proliferation of PC gaming cafés, estimated at over 100,000 nationwide, further amplifies the demand for commercial-grade peripherals that combine durability with performance.

Japan was held the second-largest position in the Asia Pacific gaming peripherals market with a share of 13.4% in 2024. As the birthplace of iconic gaming brands like Sony, Nintendo, and Bandai Namco, Japan has long been a hub for console-based and arcade-style gaming. According to the Computer Entertainment Supplier’s Association, over 60 million people in Japan engaged in regular gaming activities in 2023, many of whom relied on high-end peripherals such as custom-built keyboards, mechanical switches, and niche analog joysticks. The country is also home to some of the most influential gaming conventions, including Tokyo Game Show and Comiket, where peripheral manufacturers frequently debut prototype and limited-edition products. Companies like Astro Gaming, Elecom, and Hori have capitalized on this enthusiasm by producing locally inspired designs that blend functionality with aesthetic appeal, attracting both casual and serious gamers. Additionally, Japan’s well-established esports scene and growing adoption of virtual reality and mixed-reality gaming have spurred demand for immersive audio and haptic feedback devices. With a strong emphasis on quality, user experience, and innovation, Japan continues to be a vital contributor to the evolution of the Asia Pacific gaming peripherals market.

India is esteemed to grow lucratively with the country’s gaming ecosystem is undergoing rapid transformation, which is driven by improving internet infrastructure, rising smartphone penetration, and increasing disposable income among the youth demographic. According to the Indian Cellular and Electronics Association (ICEA), India added over 40 million new gamers in 2023, bringing the total gaming population to more than 450 million. Local e-commerce platforms like Amazon.in, Flipkart, and Reliance Digital have played a pivotal role in expanding accessibility to both global and indigenous brands. Companies like boAt, Redgear, and Zebronics have introduced affordable yet feature-rich gaming accessories tailored for budget-conscious consumers, while international players like HyperX and SteelSeries have ramped up their marketing efforts through collaborations with influencers and esports organizations.

South Korea gaming peripherals market is leveraging its reputation as a global leader in competitive gaming and digital entertainment. The country is widely recognized for its advanced broadband infrastructure, widespread adoption of esports, and deep integration of gaming into mainstream culture.

Seoul alone hosts hundreds of high-end PC cafés, known locally as “PC Bangs,” which serve as communal gaming hubs and breeding grounds for competitive talent. These establishments not only drive bulk purchases of peripherals but also serve as testing grounds for new product launches. Brands like Razer, ASUS Republic of Gamers, and Corsair have established strong footholds through sponsorships, exclusive store locations, and localized customer support programs.

Australia and New Zealand are gearing up to have prominent growth rate in the Asia Pacific gaming peripherals market in 2024. According to the Interactive Games & Entertainment Association (IGEA), over 70% of Australians engaged in regular gaming activities in 2023, with a growing percentage opting for high-fidelity peripherals to enhance their experience. The rise of streaming platforms like Twitch and YouTube Gaming has further amplified demand for microphones, webcams, and RGB-lit accessories among content creators. New Zealand, though smaller in scale, follows a similar pattern, with increasing participation in LAN events, college esports leagues, and virtual reality arcades. The New Zealand Game Developers Association reports that gaming activity among youth populations has grown steadily, with higher investment in peripherals such as mechanical keyboards and high-refresh-rate mice.

Top Players in the Market

Razer Inc. (United States-based, strong presence in APAC)

Razer is a globally recognized leader in gaming peripherals and has established a dominant footprint across the Asia Pacific region. Known for its high-performance products such as mechanical keyboards, precision mice, and immersive audio gear, Razer benefits from deep cultural alignment with gaming communities in Southeast Asia, Japan, and South Korea. The company strategically leverages its brand identity, premium aesthetics, and ecosystem integration to maintain a loyal customer base. Its localized marketing campaigns, collaborations with esports teams, and physical retail presence in key cities enhance its regional competitiveness.

Logitech G (Switzerland-based, significant operations in APAC)

Logitech G, the gaming division of Logitech, plays a pivotal role in the Asia Pacific market by offering a broad portfolio that caters to both casual and professional gamers. The company’s reputation for durable, high-quality peripherals, especially in the mouse and headset segments has earned it trust among consumers across India, China, and Australia. Logitech invests heavily in research and development, ensuring cutting-edge features such as ultra-low latency and adaptive lighting reach markets quickly.

Corsair Gaming (U.S.-based, growing influence in APAC)

Corsair has rapidly expanded its influence in the Asia Pacific gaming peripherals sector through a combination of performance-driven product design and aggressive distribution strategies. Particularly popular among PC enthusiasts in China and India, Corsair offers a wide range of customizable mechanical keyboards, RGB-lit mice, and premium headsets tailored to competitive play. The company has invested in localized e-commerce partnerships and retail expansion to better serve emerging markets. Its emphasis on system compatibility and modular upgradeability makes it a preferred choice among DIY PC builders and tech-savvy users in the region.

Top Strategies Used by Key Market Participants in the Market

Localization of Product Design and Marketing Campaigns

Key players are increasingly tailoring their product designs, branding, and promotional content to align with local gaming cultures and consumer preferences. This includes adjusting keyboard layouts for different language inputs, incorporating region-specific aesthetics, and collaborating with local influencers and esports organizations to build brand affinity. Companies like Razer and Corsair have launched limited-edition peripherals inspired by anime, K-pop, and regional gaming tournaments to deepen engagement with younger audiences in countries like Japan, South Korea, and India.

Expansion of Direct-to-Consumer and E-commerce Channels

To strengthen their regional foothold, leading brands are investing in robust online ecosystems, including branded digital stores and partnerships with major e-commerce platforms. By reducing reliance on third-party retailers, companies can offer exclusive bundles, faster delivery, and personalized after-sales support. This strategy has been particularly effective in densely populated markets like China and Indonesia, where online shopping dominates consumer behavior.

Strategic Collaborations with Game Developers and Streamers

Major gaming peripheral manufacturers are forging partnerships with game studios and top-tier streamers to co-develop products optimized for specific games or streaming environments. These collaborations not only drive visibility but also ensure that peripherals meet the technical demands of popular titles and livestreaming workflows. Brands are leveraging these relationships to reinforce their image as essential tools for elite performance and community engagement.

COMPETITION OVERVIEW

The competition in the Asia Pacific gaming peripherals market is intense and multifaceted, shaped by a mix of global giants, regional powerhouses, and agile startups vying for consumer attention. Established international brands such as Razer, Logitech G, and Corsair dominate with their advanced technologies, extensive product lines, and strong brand recognition. However, they face growing pressure from emerging domestic players who offer cost-effective alternatives with localized appeal. In markets like China, India, and Southeast Asia, affordability and customization are becoming key decision-making factors, prompting even global firms to introduce budget-friendly models under sub-brands or partner with local distributors.

Technology innovation plays a crucial role in maintaining competitive differentiation, especially in areas such as wireless connectivity, ergonomic design, and software integration. Companies are racing to incorporate low-latency solutions, modular components, and AI-enhanced features into their offerings. At the same time, marketing strategies are evolving beyond traditional advertising to include influencer endorsements, esports sponsorships, and user-generated content campaigns aimed at engaging younger demographics.

E-commerce dynamics are further intensifying rivalry, as brands compete for visibility on platforms like Amazon, Shopee, and Lazada. With price wars, bundled deals, and rapid product cycles becoming the norm, companies must continuously innovate and adapt to stay ahead. As the Asia Pacific gaming culture continues to mature, the battle for market dominance will hinge on a delicate balance between technological superiority, cultural relevance, and operational agility.

RECENT HAPPENINGS IN THE MARKET

- In March 2024, Razer announced the launch of its first flagship concept store in Singapore, featuring interactive product displays, custom-built demo stations, and live esports event screenings. This initiative was designed to deepen consumer engagement and elevate the brand’s experiential retail presence in Southeast Asia.

- In June 2024, Logitech G partnered with a leading Korean esports organization to co-develop a line of gaming mice and headsets tailored for League of Legends and Valorant players, enhancing performance metrics aligned with competitive gameplay requirements in the APAC region.

- In September 2024, Corsair opened a new regional logistics hub in Bangalore, India, aimed at improving supply chain efficiency and reducing lead times for online orders, especially during peak sales periods such as festive shopping seasons and gaming festival weekends.

- In November 2024, Redragon, an Australian-based gaming peripherals brand, entered into a strategic partnership with a Japanese electronics retailer to expand its offline retail presence, making its budget-focused gaming keyboards and mice more accessible to local consumers.

- In January 2025, SteelSeries collaborated with a major Chinese livestreaming platform to introduce a co-branded line of studio-grade microphones and RGB lighting kits specifically designed for content creators, targeting the booming live-streaming and influencer economy in the Asia Pacific region.

MARKET SEGMENTATION

This research report on the Asia Pacific gaming peripherals market is segmented and sub-segmented into the following categories.

By Product Type

- Headsets

- Keyboards

- Joysticks

- Mice

- Gamepads

- Others

By Gaming Device Type

- PC (Desktop/Laptop)

- Gaming Consoles

By Technology

By Distribution Channel

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

At CES 2026, Akko calls attention to three distinct series — the Nest, the Dash, and the Framer. The brand highlights the Dash as its “most advanced mouse to date.” This computer peripheral weighs just 39 grams and boasts the PixArt 3950 sensor for ro-grade precision and stability. Nest, on the other hand, is a right-hand ergonomic style, while the Framer is for entry-level gaming.

In addition to the high-performance computer mice, Akko is also highlighting new keyboards — including the aluminum rapid assembly magnetic-switch keyboard MOD007v5 HE and the Year of the Snake Keyboard — as well as the M1 V5 TMR technology by Akko’s sister brand MonsGeek.

Image Credit: Akko

Gambling Industry Trends and Predictions for 2026

The global gambling industry enters 2026 on a rapid growth trajectory and at the cusp of transformative change. After reaching an estimated $99 billion in 2024, the global betting and gaming market is projected to nearly double by 2033 (approaching $182 billion) as digital platforms, mobile betting, and AI-driven innovations reshape how people gamble. This boom is fueled not only by technological leaps, but also by evolving consumer behaviors and shifting regulatory landscapes. By 2026, the industry will be more connected, data-driven, and consumer-focused than ever, blurring the line between gambling and broader digital entertainment.

Global Focus, Local Moves: North America and Europe currently dominate gambling revenue (about three-quarters of the market), but Asia-Pacific and Latin America are emerging as the next frontiers. In particular, Asia-Pacific’s liberalizing regulations, rising incomes, and mobile adoption are accelerating participation across the region. At the same time, the United States – which ignited a sports betting boom after 2018 – continues to expand state-by-state. Meanwhile, Europe’s mature markets are prioritizing sustainability and responsibility, and Latin America and Africa are opening up new opportunities. Across the world, stakeholders are “going all-in” on innovation and expansion, while bracing for greater oversight to ensure gambling grows safely.

In this outlook for 2026, we highlight the key trends shaping the iGaming (online gambling) sector and its convergence with traditional brick-and-mortar casinos. From new markets and regulations to tech breakthroughs and changing player expectations, the year ahead promises high stakes and big opportunities.

New Markets and Regulatory Shifts on the Horizon

Legalization Wave Continues

The map of regulated gambling is set to expand further in 2026. Several countries and jurisdictions are transitioning from gray markets to fully legal, competitive industries. Notably, Brazil – long considered a “sleeping giant” of gaming – is rolling out regulations for online sports betting and casino gaming, creating one of the world’s largest new markets. In Europe, Finland has decided to end its state monopoly and move toward a competitive licensing model by 2026, opening its lucrative market to private iGaming operators. These moves follow the trend of governments seeking tax revenue and consumer protection through licensing rather than prohibition.

United States Focus

In the U.S., the sports betting frenzy that spread to 35+ states is settling into a mature phase, but there are still holdouts and new opportunities. Major states like Texas and California remain unresolved – Texas lawmakers are weighing another push for sportsbooks (though realistically not before 2027) and California’s tribal vs. commercial interests make legalization challenging. Still, the pressure is mounting as Americans in nearly every region have gained access to legal betting.

Meanwhile, online casino gaming (iGaming) – currently legal in only seven states – is gaining traction. In 2025, multiple U.S. states saw legislative efforts to legalize online casinos, eyeing the success of pioneers like New Jersey, Michigan, and Pennsylvania. The record-breaking revenues reported by existing iGaming states underscore the opportunity: several markets have posted all-time monthly records, and year-over-year growth in iGaming has significantly outpaced growth in brick-and-mortar casinos. This momentum is likely to push more U.S. states to consider regulating online casinos in 2026 and beyond, especially as they watch neighbors reap tax windfalls.

Stricter Rules and Compliance

As new markets open, regulators everywhere are also tightening the rules in existing markets. Governments in major jurisdictions are introducing tougher measures for consumer protection, anti-money-laundering (AML), and advertising. The United Kingdom’s regulatory overhaul is a prime example – from stricter ad guidelines to potential online slot stake limits and affordability checks, UK operators face a more controlled environment. Other countries have gone so far as to heavily restrict or ban gambling advertising. Across Europe, compliance is king: the era of “grey area” operations is fading as authorities push operators to either go fully legal or get out.

In the U.S., regulators are aggressively enforcing rules to ensure a safe market. Several states have intensified enforcement against unlicensed platforms, increased cease-and-desist activity, and introduced new rule updates emphasizing tighter licensing standards, identity verification, AML protocols, and mandatory responsible gambling tools. This reflects a broader North American trend: as the online market matures, regulators are shifting from simply enabling new industries to rigorously policing them for compliance and strengthening player protections.

Tax and Policy Changes

Policymakers are also adjusting the financial rules around gambling. In the U.S., a notable change takes effect in 2026: recreational gamblers will lose a portion of their tax deductions on losses, with federal law capping deductible losses at 90% of winnings (down from 100%). This tax tweak may discourage some high-volume bettors or at least complicate their accounting. At the same time, U.S. reporting thresholds for certain jackpots have been modernized in recent years, reflecting a slow but steady effort to update outdated compliance burdens.

Overall, 2026’s regulatory landscape will be defined by expansion paired with vigilance: more markets opening up and more scrutiny to ensure gambling growth comes with strong consumer safeguards. Next, we look at one of the most intriguing regulatory battles brewing – the clash between traditional gambling operators and a new breed of betting platform known as prediction markets.

A major storyline heading into 2026 is the rise of prediction markets and their collision with traditional sports betting. Once a niche idea, prediction markets allow users to wager on practically any real-world outcome – from elections and economic indicators to pop culture outcomes – treating events like stocks to be traded. In the past two years, this segment expanded rapidly in the United States, blurring the line between gambling and financial trading. A growing roster of platforms has launched or gone mainstream, and major sports and gaming brands are experimenting with prediction-style products.

This flurry of innovation points to demand for new forms of interactive wagering. Younger bettors especially enjoy the stock-market-like experience of trading event outcomes, and volumes have surged across several platforms. These numbers have not gone unnoticed by the traditional gaming industry – or by its regulators.

Regulatory Crossfire

Prediction markets currently operate in a legal gray area in the U.S., often falling under federal commodities oversight rather than state gambling law. This has triggered backlash from established gambling stakeholders who argue these products resemble sports betting without the same level of licensing, consumer protection, and responsible gaming guardrails.

On the other side, prediction market companies and allied fintech firms are organizing and pushing for clearer frameworks that legitimize these markets nationwide. They argue that the legal system hasn’t kept pace with modern products, and that a patchwork of rules will create confusion and drive demand to offshore alternatives. The stage is set for a significant confrontation in 2026: federal regulators vs. state gaming authorities, and innovative platforms vs. incumbent casino and sportsbook ecosystems.

Why This Matters in 2026

Whether prediction markets are integrated into the regulated gaming system, restricted, or forced into separate lanes will shape everything from taxation and consumer protections to how sportsbooks innovate. The industry may be moving toward a reality where traditional operators either (1) partner into this category, (2) fight it aggressively, or (3) watch parts of wagering demand shift outside classic sportsbook rails. The outcome won’t just impact the U.S.; it will influence global regulators as they face similar fintech-gambling convergence pressures.

The Great Convergence: Merging iGaming with Brick-and-Mortar Casinos

The year 2026 will also highlight the convergence between online and land-based gambling, often dubbed the “omnichannel” approach. While online iGaming is booming, traditional physical casinos are not standing idle – many are leveraging technology and cross-platform strategies to stay relevant and connected to digital audiences. The central question for casino operators has become: How can we integrate the on-site casino experience with online play?

Omnichannel Strategies

Some forward-thinking casino companies are embracing hybrid innovations that turn brick-and-mortar resorts into content engines for digital channels. New live dealer concepts, broadcast-style casino content, and in-property studios are becoming a real strategy: they extend a casino brand beyond physical walls while turning on-site foot traffic into marketing reach.

Another critical driver of convergence is the integration of loyalty programs and currencies across channels. Big operators are linking loyalty points so that players earn and spend rewards whether they’re at a slot machine in Vegas or betting on an app at home. Increasingly, these rewards behave more like digital ecosystems than simple points programs. Over time, this may evolve toward a portable digital identity where engagement across sportsbook, casino, social gaming, and entertainment can be recognized and rewarded holistically.

Physical Casinos Go Digital

Brick-and-mortar casinos are also adopting more digital infrastructure: cashless wagering options, mobile wallets, app-driven player experiences, and increasing experimentation with biometrics for identity and loyalty recognition. These upgrades align with younger customers’ expectations and help casinos enhance operational efficiency while reducing certain fraud and compliance risks.

It’s worth noting that not all casino operators are on board. Some U.S. regional casino companies and tribal stakeholders remain cautious, citing cannibalization concerns and social impacts. Still, the broader revenue picture continues to pressure the industry toward convergence, especially as online channels deliver faster growth and higher scalability.

The “Phygital” Casino Experience

In 2026, expect to see more crossover initiatives that make gambling an anytime, anywhere activity. The convergence is also evident in content: casino games increasingly borrow features from video games (missions, rewards loops, community events), while physical casinos adopt attractions influenced by digital culture. For operators, the strategic advantage goes to whoever can unify experiences across platforms while respecting the regulatory and responsible gaming frameworks required in each market.

Tech Innovations: AI, Apps, and Immersive Betting

Technology has always been a driving force in iGaming, but heading into 2026, it’s clear the industry is entering another innovation cycle. Several tech trends are set to redefine how gambling products are built and how players engage:

Mobile 2.0 – Faster and More Immersive

Mobile betting is the primary channel for many consumers, and in 2026 mobile platforms are leveling up. Expect smoother UX, deeper personalization, more embedded live content, and early-stage applications of AR to create more immersive experiences. The smartphone is not just a portal to betting anymore; it’s becoming the interface layer for entertainment, payments, community, and identity.

Artificial Intelligence Everywhere

AI has moved from experimentation to operational core. It is now embedded in risk management, fraud detection, dynamic promotions, personalization, customer support, and even content generation. The next stage in 2026 is “industrialized AI”: measurable ROI, tighter governance, and clearer outcomes. In regulated markets, AI will increasingly be paired with compliance expectations – including systems designed to detect problem gambling behaviors earlier and deliver better interventions.

Fintech and Payments Innovation

Payments are becoming a strategic battleground. Open banking capabilities, faster payouts, improved fraud detection, and easier onboarding are changing player expectations. In parallel, crypto rails remain relevant, especially for international markets and certain user segments. For regulated operators, the key is not crypto hype, but crypto’s utility: faster settlement, transparent transaction trails, and optionality for global payments where traditional banking remains restrictive.

New Game Formats – eSports, Virtuals, and Microbets

New formats continue to expand the addressable audience. eSports betting is growing, virtual sports offer always-on wagering, and micro-betting is becoming a major engagement driver as operators refine the latency, data feeds, and in-play UX that this product demands. Major global sporting events in 2026 will likely accelerate micro-betting adoption as consumers learn to treat a match not as one bet, but as dozens of moment-to-moment decision points.

Gamification and Social Play

Gamification is now a baseline expectation in modern apps: missions, rewards, leaderboards, community challenges, and social layers that borrow heavily from video games. Meanwhile, streaming culture continues to collide with iGaming, as content creators, live casino formats, and interactive “watch and play” mechanics become more common acquisition channels. As these experiences scale, expect regulators to sharpen the rules around marketing, affiliate behavior, and ensuring responsible gaming protections extend into creator-led environments.

Cybersecurity and Reliability

As platforms scale, cybersecurity becomes existential. Attacks, phishing, and platform reliability issues can quickly damage trust. In 2026, regulators and major partners will increasingly treat security readiness and resilience as non-negotiable. Operators will invest further in multi-cloud uptime strategies, monitoring, and stronger identity protections to ensure stable, compliant operations at scale.

Responsible Gambling and the Social License

Amid all the growth and innovation, the industry in 2026 is putting a sharper focus on responsible gambling (RG). As gambling becomes more accessible digitally, the expectations rise: operators must prevent harm, regulators must protect consumers, and stakeholders must prove that industry growth can be sustainable.

Real-Time Intervention

One of the most important evolutions is the use of AI and behavioral analytics to detect harmful patterns earlier. Instead of relying solely on players to self-report or set limits, modern systems can identify risk signals and trigger interventions such as dynamic messaging, cooling-off prompts, or structured friction in the user journey.

Mandatory Measures and Culture Change

More jurisdictions are tightening requirements: deposit and time limits, self-exclusion enforcement, clear loss/win displays, enhanced KYC checks, and more robust proof-of-source-of-funds rules in higher-risk cases. The direction is clear: responsible gambling is no longer optional, and the companies that build it into product design will find it easier to keep market access, maintain brand trust, and partner with mainstream institutions.

The challenge is that responsible gambling messaging must be effective, not performative. Generic slogans are losing impact. The next phase is more personalized, contextual, and integrated into product design without creating a punitive experience for recreational users.

Conclusion: 2026 and Beyond – A High-Tech, High-Responsibility Future

The year 2026 is poised to be a pivotal chapter for iGaming and the casino industry, marked by convergence and innovation on one hand, and heightened responsibility and regulation on the other. We will see new markets expand, the U.S. inch closer to broader iGaming adoption, and regulators increasingly demand stronger safeguards as online access becomes ubiquitous.

India’s gaming industry is rapidly evolving into one of the largest and most dynamic markets in the world. Driven by the increasing adoption of smartphones, affordable internet, and a tech-savvy youth population, gaming is becoming a mainstream form of entertainment. With mobile gaming leading the charge, the India gaming market is also witnessing significant growth in esports, cloud gaming, and immersive technologies like augmented reality (AR) and virtual reality (VR).

Unlocking New Realms: The Evolution and Key Opportunities in India’s Gaming Sector

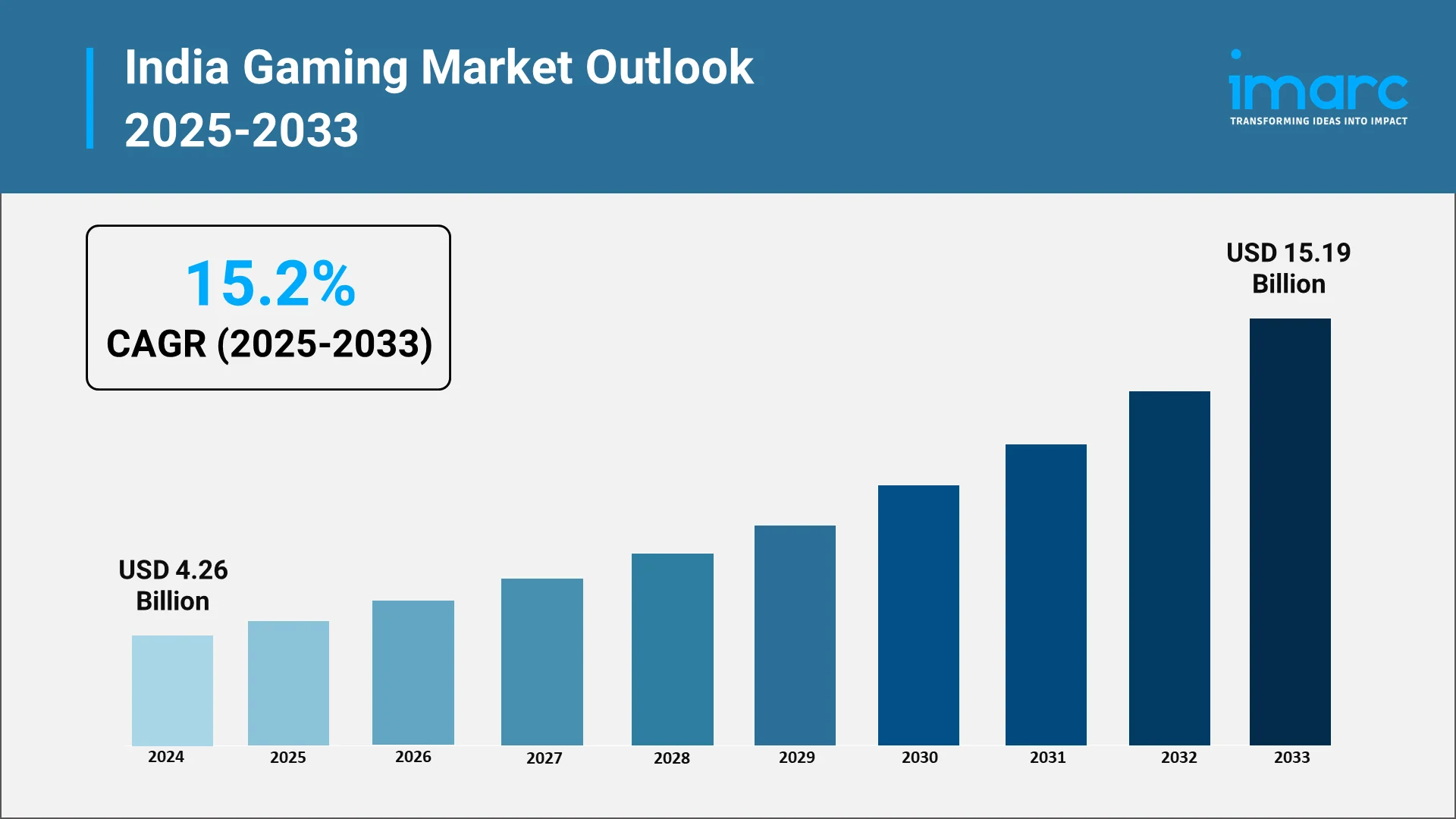

The gaming sector is transitioning from a specialized sector to a dynamic and swiftly growing market, fueled by the rising use of smartphones, accessible internet, and a young, tech-oriented demographic. The rise of mobile gaming is at the heart of this transformation, with millions of people in India engaging in gaming on their smartphones daily. With the nation’s gaming industry growing, a variety of gamers, covering mobile, console, and PC platforms, are shaping the industry. Quantifying this rapid expansion, the IMARC Group reported that the gaming market size in India reached USD 4.26 Billion in 2024.

The primary opportunities ahead are in the rising need for localized content, as developers are concentrating on designing games that connect with Indian cultural and regional tastes. This presents substantial potential to reach a broader audience, especially in tier-2 and tier-3 cities. Moreover, the growth of esports, cloud gaming, AR, and VR technologies offers new opportunities for expansion. With the growing investment and support from both the government and private sectors, there is significant potential to establish India as a worldwide center for gaming development and creativity.

With the market’s maturation, the advancement of monetization strategies, enhanced infrastructure, and stronger regulations will continue to contribute to the increase in India gaming market share, unlocking untapped potential and fostering global competitiveness.

Explore in-depth findings for this market, Request Sample

Game On: Current Trends and Market Drivers Shaping India’s Gaming Future

According to IMARC Group’s projections, the India gaming market is projected to grow at a CAGR of around 15.2% from 2025 to 2033, reaching USD 15.19 Billion by 2033. The growth will be supported by the following factors:

- Smartphone and Internet Penetration

India’s increasing number of affordable smartphones, coupled with the expansion of high-speed internet access, is significantly broadening the market reach. As rural and non-metro areas gain improved connectivity, companies can target new user segments beyond urban centers. This growing accessibility enables casual, on-the-go gaming, contributing to a surge in user numbers and expanding the market. As of March 2024, India had 954.40 million total internet subscribers, with 398.35 million rural subscribers. Furthermore, by April 2024, 95.15% of India’s 644,131 villages were equipped with 3G/4G mobile connectivity, underscoring the increasing digital penetration across the country and creating vast opportunities for gaming expansion in rural areas.

- Monetization Evolution: In–App, Subscription & Cloud

The monetization models in the gaming market in India are evolving beyond basic in-app purchases. Traditional in-app purchases are being complemented by subscription models, cloud streaming, and cross-platform play, providing new revenue streams and catering to players seeking more flexibility and value. This shift allows gaming companies to offer premium experiences while enhancing player lifetime value. A prime example of this trend is Nvidia’s announcement in 2025 that its GeForce NOW cloud gaming service will launch in India, offering high-end gaming experiences on various devices. Premium members can access over 4,500 games, including popular titles like Borderlands 4 and Call of Duty: Black Ops 7, solidifying cloud gaming’s potential in India.

- Esports Partnerships and Innovation

A key factor driving the growth of the market is the increasing investment in esports partnerships and innovation. Realme’s collaboration with Krafton India as the official smartphone partner for the BattleGrounds Mobile Series (BGIS) 2025 and BGMI Pro Series (BMPS) 2025 highlights this trend. By using its GT 7 Pro for the tournaments, Realme is directly supporting both professional and grassroots players. This partnership not only boosts esports visibility but also strengthens the gaming ecosystem in India. As esports continues to gain traction, such collaborations enhance the gaming experience and contribute to market expansion.

- Localized Product Offerings and Market Tailoring

The growing availability of localized products tailored to the needs of Indian gamers is positively influencing the market. Acer’s announcement in 2025 to launch “Make in India” gaming laptops is a prime example. By customizing its Aspire/ALG, Nitro, and Predator series for the Indian market, Acer is addressing the performance, pricing, and usage patterns unique to Indian gamers. This move not only supports the rising demand for gaming PCs across casual, competitive, and creator segments but also taps into the rising interest in AI-ready devices, contributing to the rapid expansion of India’s gaming ecosystem.

The rise of accelerator programs and funding initiatives is helping local developers access advanced technology, mentorship, and global networks. The adoption of AI tools is particularly transformative, enhancing game development, player experiences, and monetization strategies. These AI-driven innovations improve gameplay mechanics, automate processes, and offer personalized content, making Indian games more competitive globally. A prime example is Meta’s India-focused Gaming Accelerator, launched in 2025, which supports 20–30 emerging studios with AI tools like Llama, along with mentorship and investor access to scale their games for global markets.

The Game Plan: Conquering Challenges and Unlocking New Opportunities

The Indian gaming industry encounters challenges like regulatory ambiguity, with many states lacking clear rules for online gaming, creating confusion for developers and players. The country’s vast and diverse population also requires significant investment in localization and culturally relevant content. Additionally, piracy and data security concerns remain persistent threats.

Despite these obstacles, the rapid increase in internet access and smartphone adoption, particularly in tier-2 and tier-3 cities, presents a large untapped market. Mobile gaming is becoming popular because of affordable smartphones and data plans, while localization offers a chance to engage diverse user bases. The growing momentum of the India Mobile Gaming Market further highlights how digital engagement is expanding across demographic groups. Esports and online competitions are also gaining traction, creating new opportunities for competitive gaming and sponsorships.

Masters of the Game: Who’s Leading India’s Gaming Industry

Major figures in the market are progressively concentrating on broadening their reach and enhancing user interaction by utilizing mobile-first approaches and integrating localized content. These firms are focusing on creating games that align with local tastes, providing content in various languages and crafting gameplay that reflects India’s rich cultural diversity. Numerous developers are investigating fresh monetization strategies, such as in-app purchases, subscription models, and live events, while incorporating social and multiplayer elements to promote community engagement. To remain competitive, they are significantly investing in technology like AI and cloud gaming to improve user experiences and provide smooth cross-platform play. Directly illustrating the investment in technology like cloud gaming to improve user experiences and provide smooth cross-platform play, Xbox launched cloud gaming in India for Game Pass subscribers in 2025, allowing high-end games to stream on mobiles, tablets, and PCs.

.webp)

The Game Changers: How Investment and Government Support Are Elevating the Gaming Sector

The gaming market in India is influenced by government-backed initiatives and a clear regulatory framework that foster innovation and growth. These programs support game design, development, and talent, attracting both local and global investments. The regulatory system ensures fair practices and transparency, building market trust and safeguarding user interests.

- Government-backed programs are essential in driving innovation and creating a vibrant gaming ecosystem in India. By supporting game design, development, and talent nurturing, these initiatives provide infrastructure, networking, and industry collaboration that attract both local and global investments. They also focus on cultivating local talent, ensuring the sector’s sustainability and competitiveness. The government’s commitment is evident in major initiatives like the Create in India Challenge and the AVGC-XR Mission, launched in 2025, which aim to foster original creation and collaboration across gaming, animation, VFX, and immersive technologies. These efforts strengthen India’s creative economy and position the country as a global hub for AVGC-XR innovation.

- A coherent regulatory system is vital for driving the gaming market in India. By establishing clear rules and categories for different game types, such as esports and online gaming, the framework ensures transparency and fair practices, fostering trust among investors and participants. This organized approach enhances market security for both developers and users, promoting sustainable growth. In 2025, the Ministry of Electronics and Information Technology (MeitY) addressed the need for such a framework with the release of the Draft Promotion and Regulation of Online Gaming Rules under the PROG Act. This created India’s first unified framework, with the Online Gaming Authority overseeing compliance, classification, and registration.

Leveling Up: IMARC’s Playbook for Navigating India’s Thriving Gaming Market

IMARC Group empowers stakeholders in India’s gaming industry with data-driven insights to succeed in one of the world’s fastest-growing entertainment markets. Our research and consulting services help clients identify untapped opportunities, navigate market uncertainties, and drive innovation in game design, marketing, and retail strategy.

- Market Insights: Track trends shaping India’s gaming market, including the rise in mobile gaming, increasing demand for esports, and the growing popularity of educational and strategy-based games. We also explore the emergence of local developers and the expanding gaming ecosystem.

- Strategic Forecasting: Predict future developments in the integration of digital and physical gaming experiences, the growth of online gaming platforms, evolving user preferences, and the impact of regional content and culturally relevant game narratives.

- Competitive Intelligence: Analyze strategies and offerings from leading game publishers and emerging startups, including how they are redefining gaming experiences with local themes, storytelling, and sustainable production practices.

- Policy and Regulatory Analysis: Understand trade regulations, intellectual property protection, licensing, and safety compliance standards crucial to the production and distribution of games in India.

- Tailored Consulting Solutions: Benefit from customized advice on market entry strategies, distribution models, branding, and game localization. IMARC’s expertise supports businesses in developing scalable, client-centric growth strategies in an expanding gaming ecosystem.

The New Nevada Gaming Board Chairman knows the importance of getting technology OK’d quickly, signaling a clear focus on modernizing how gaming innovations move from development to casino floors. This approach reflects an understanding that technology now plays a central role in the gaming industry and that regulatory systems must evolve to keep Nevada competitive while maintaining its high standards.

New Chairman Knows the Importance of Approving Technology

Gaming technology is advancing at a rapid pace, from new slot machine platforms to cashless systems and enhanced security tools. When approvals take too long, Nevada risks seeing new products debut elsewhere first. The New Nevada Gaming Board Chairman knows the importance of getting technology approved quickly because delays can affect manufacturers, casino operators, and ultimately the state’s position as a leader in regulated gaming.

Industry Experience Shaping Regulatory Priorities

Leadership matters in regulatory agencies, especially in industries as complex as gaming. The new chairman brings experience that bridges regulation and technology, offering insight into how long approval timelines can impact innovation. This background helps explain why the New Nevada Gaming Board Chairman knows the importance of getting technology OK’d quickly, not as a shortcut, but as a way to make processes more efficient and predictable.

How Faster Approvals Benefit Nevada’s Gaming Industry

Timely technology approvals help casinos remain competitive and allow players to experience the latest advancements sooner. When Nevada can approve new gaming systems without unnecessary delays, it strengthens relationships with manufacturers and reinforces the state’s reputation as the global standard for gaming regulation.

Maintaining Integrity While Moving Faster

Speed does not mean sacrificing oversight. Nevada’s gaming regulators are still responsible for ensuring fairness, security, and compliance. The emphasis is on refining internal processes, improving communication, and reducing bottlenecks. This balanced approach explains why the Nevada Gaming Board Chairman knows the importance of getting technology approved quickly while continuing to uphold strict regulatory safeguards.

What This Means for the Future of Gaming Regulation

Looking ahead, a more responsive approval process could encourage greater innovation within Nevada’s gaming sector. Developers may be more inclined to launch new technologies in the state, and operators can adapt more quickly to player expectations.

By aligning regulatory efficiency with technological progress, Nevada positions itself to remain both a trusted regulator and an innovation-friendly environment in an increasingly competitive global gaming market.

Looking for Legal Guidance in Gaming?

If you follow SCCG content and have inquiries about your gaming business, connect with Lazarus Crystal Law Firm—formed by SCCG Management and Lazarus Legal to unite top-tier gaming law with commercialization and market-entry strategy.

Our Areas of Expertise Include:

• Nevada and multi-state gaming licensing

• Regulatory compliance and audit services

• International market entry and cross-border advisory

• Gaming M&A legal due diligence

• Tribal gaming legal and strategic support

• iGaming and sports betting regulatory guidance

Follow us on LinkedIn: Lazarus Crystal Law Firm

Samsung Electronics has unveiled its new most advanced Odyssey gaming monitor lineup. The lineup includes five new models that push the boundaries of resolution, refresh rates, and immersive visual performance.

Led by Samsung’s first 6K 3D Odyssey G9, the 2026 lineup debuts world-first display technologies for gamers and creators, including the next-generation Odyssey G6 and three new Odyssey G8 models.

First 6K glasses-free 3D monitor

“With this year’s Odyssey lineup, we’re introducing display experiences that simply weren’t possible even a year ago,” said Hun Lee, Executive Vice President of the Visual Display (VD) Business at Samsung Electronics.

“From the industry’s first 6K glasses-free 3D monitor to breakthrough 1,040Hz speed, we designed these monitors to meet the ambitions of today’s gamers and deliver a level of immersion that fundamentally changes how content looks and functions on screen.”

The 32-inch Odyssey 3D (G90XH model) debuts the world’s first 6K display with glasses-free 3D, introducing a new way to experience games on a monitor. Powered by real-time eye tracking, it adjusts depth and perspective in response to the viewer’s position, creating a layered sense of dimension for smooth, uninterrupted gameplay without the need for a headset, according to a press release.

PC gamers can enjoy high-quality expanded lineup

With 6K resolution, a 165Hz refresh rate boosted to 330Hz through Dual Mode, and 1ms response time, fast action stays sharp and smooth, according to Samsung.

The company claims that PC gamers can enjoy a high-quality expanded lineup of supported titles with optimized 3D effects developed in collaboration with game studios. Featured games such as The First Berserker: Khazan, Lies of P: Overture, and Stellar Blade will offer added dimensionality, enhancing terrain, distance, and object separation beyond standard 2D gameplay.

The South Korean company has also highlighted that the 27-inch Odyssey G6 (G60H model) gaming monitor advances competitive gaming with the world’s first 1,040Hz gaming monitor through Dual Mode and native QHD support up to 600Hz, delivering esports-level motion clarity to help players track targets and see fine details during high-speed movement.

When needed, the Odyssey G6 can boost performance in an instant, providing ultra-sharp resolution so viewers can experience breathtaking worlds and ultra-high speeds that fuel competitive adrenaline. With support from both AMD FreeSync Premium and NVIDIA G-Sync Compatible, the Odyssey G6 ensures that every frame is smooth, every color pops, and every moment feels responsive.

The Odyssey G8 series is expanding in 2026 with three distinct models, each offering a different balance of resolution and speed. Leading the lineup, the 32-inch Odyssey G8 (G80HS model), the industry’s first 6K gaming monitor, delivers native 165Hz performance with Dual Mode that supports up to 330Hz in 3K mode.

The 27-inch Odyssey G8 (G80HF model) offers a sharper 5K option with native support up to 180Hz, and Dual Mode boosts to 360Hz in QHD for smoother motion.

For users who want deeper contrast, the 32-inch Odyssey OLED G8 (G80SH model) pairs a 4K QD-OLED panel with a 240Hz refresh rate, Glare Free viewing, 300-nit brightness, and VESA DisplayHDR True Black 500 certification. Its DisplayPort 2.1 (UHBR20) supports up to 80 Gbps of bandwidth for seamless HDR and VRR playback, according to Samsung.

The complete Odyssey 2026 lineup will be on display at CES 2026 in Las Vegas from January 6-9.

Is Missouri football close to landing transfer portal QB? Reports say so

Coach turns backyard into 80-foot ice rink each year to serve youth hockey team

Kent City Council gets update about YMCA operations

Logan Sargeant’s Transition to Endurance Racing

Innovative Gaming Peripheral Ecosystems : gaming peripheral

H.S. Roundup: Area indoor track athletes compete at PVIAC meet No. 3

Real Madrid Foundation Holds Camp at Burbank High

College football transfer tracker: With portal now open, where will top players end up?

SEC team linked to star transfer WR Cam Coleman

Texas WR Parker Livingstone to enter the NCAA transfer portal

MVB Opens 2026 Season Saturday with Home Contest Versus Trine

College football season now guaranteed a happy ending, plus it’s portal time

Sign Up for Volleyball Skills Training at Biltmore Hills Community Center

Case, Somerset Berkley Thanksgiving football rivalry is back

Creighton volleyball gets Wisconsin player from transfer portal

SoundGear Named Entitlement Sponsor of Spears CARS Tour Southwest Opener

Donny Schatz finds new home for 2026, inks full-time deal with CJB Motorsports – InForum

Black Bear Revises Recording Policies After Rulebook Language Surfaces via Lever

David Blitzer, Harris Blitzer Sports & Entertainment

How Donald Trump became FIFA’s ‘soccer president’ long before World Cup draw

DeSantis Talks College Football, Calls for Reforms to NIL and Transfer Portal · The Floridian

Elliot and Thuotte Highlight Men’s Indoor Track and Field Season Opener

JR Motorsports Confirms Death Of NASCAR Veteran Michael Annett At Age 39

#11 Volleyball Practices, Then Meets Media Prior to #2 Kentucky Match

Rick Ware Racing switching to Chevrolet for 2026

Colleges ponying up in support of football coaches, programs

West Fargo volleyball coach Kelsey Titus resigns after four seasons – InForum

Nascar legal saga ends as 23XI, Front Row secure settlement

Maine wraps up Fall Semester with a win in Black Bear Invitational

Ross Brawn to receive Autosport Gold Medal Award at 2026 Autosport Awards, Honouring a Lifetime Shaping Modern F1

-

Motorsports2 weeks ago

Motorsports2 weeks agoRoss Brawn to receive Autosport Gold Medal Award at 2026 Autosport Awards, Honouring a Lifetime Shaping Modern F1

-

Rec Sports2 weeks ago

Rec Sports2 weeks agoPrinceton Area Community Foundation awards more than $1.3 million to 40 local nonprofits ⋆ Princeton, NJ local news %

-

Rec Sports3 weeks ago

Rec Sports3 weeks agoStempien to seek opening for Branch County Circuit Court Judge | WTVB | 1590 AM · 95.5 FM

-

NIL3 weeks ago

NIL3 weeks agoDowntown Athletic Club of Hawaiʻi gives $300K to Boost the ’Bows NIL fund

-

NIL2 weeks ago

NIL2 weeks agoKentucky AD explains NIL, JMI partnership and cap rules

-

Rec Sports3 weeks ago

Rec Sports3 weeks agoTeesside youth discovers more than a sport

-

Motorsports3 weeks ago

Motorsports3 weeks agoPRI Show revs through Indy, sets tone for 2026 racing season

-

Sports3 weeks ago

Sports3 weeks agoYoung People Are Driving a Surge in Triathlon Sign-Ups

-

Sports3 weeks ago

Sports3 weeks agoThree Clarkson Volleyball Players Named to CSC Academic All-District List

-

Sports3 weeks ago

Sports3 weeks agoCentral’s Meyer earns weekly USTFCCCA national honor